Ethiopia Economic Update by African Development Bank- Ethiopia’s economy grew by 6.1% in 2020, down from 8.4% in 2019, largely because of the COVID–19 pandemic. Growth was led by the services and industry sectors, whereas the hospitability, transport, and communications sectors were adversely affected by the pandemic and the associated containment measures to prevent the spread of the virus.

The fiscal deficit, including grants, increased slightly during 2020, financed mainly by treasury bills. Tax revenue increased by 16%, but the tax-to-GDP ratio declined to 9.2% in 2020 from 10% in 2019 due to delayed implementation of tax reforms. Total public spending remained stable, in line with the country’s fiscal consolidation strategy.

In 2020 inflation reached 20.6%, well above the 8% target, due to pandemic-induced supply chain disruptions and expansionary monetary policy. In November 2020, the official exchange rate was devalued by about 8% to 35.0 birr per US dollar. Export revenues increased by 12% in 2020, as exports of gold, flowers, coffee, and chat increased while imports declined by 8.1%.

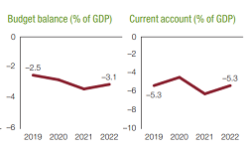

This helped narrow the current account deficit to 4.4% in 2020 from 5.3% in 2019. Service sector exports declined by about 6%, mostly because of lower revenue from Ethiopian Airlines. Foreign direct investment (FDI) fell 20% to 2.2% of GDP, and personal remittances declined by 10% to 5.3% of GDP. Poverty was projected to decline from 23.5% in 2016 to 19% by end of 2020. But pandemic-driven job losses, estimated at as many as 2.5 million, will impede poverty reduction.

Outlook and risks

The medium-term economic outlook is contingent on the resolution of the COVID–19 crisis, the pace of the economic recovery, and such other shocks as civil strife and climate change. Real GDP growth in 2021 is projected to fall to 2%, then recover to about 8% in 2022, led by a rebound in industry and services. Monetary policy is expected to remain flexible in response to the government’s financing requirements.

Increased use of open-market operations is expected to reduce inflation gradually. The fiscal deficit is projected to increase as tax policy reforms are delayed due to COVID–19. The current account is likely to deteriorate in 2021 before improving in 2022 as service exports gradually pick

up.

The key downside risks to the economic outlook include low investor confidence, in part due to sporadic domestic conflicts, weakness in global growth, and climate change.

Financing issues and options

Ethiopia’s financing requirements are significant given its large physical and social infrastructure needs and low tax-to-GDP ratio, which averaged 10% from 2017 to 2020. The primary deficit plus debt service was estimated at nearly 4% of GDP. As of June 2020, total public debt was about 57% of GDP, slightly more than half of which was external.

Since 2017, Ethiopia has been classified at high risk of public debt distress due to weak export performance coupled with increased import-intensive public infrastructure investments. The International Monetary Fund’s 2019 debt sustainability analysis estimated the net

present value of debt-to-exports at 247.6% and debt service-to-exports at 24.6%; the highest sustainable levels are 180% and 15%, respectively.

Ethiopia benefited from the G20 Debt Service Suspension Initiative, and the government is taking measures to contain the debt burden as part of the so-called Home-Grown Economic Reform

agenda, which includes fiscal consolidation, expanding public financing sources, a moratorium on nonconcessional borrowing, harnessing grants and concessional loans, and debt restructuring.

Gross reserves amounted to $3.1 billion in 2020, or 2.5 months of imports and are unlikely to provide an alternative source of development financing in the short term.

Expansion of public debt in the context of large public expenditure requirements could constrict the fiscal space and lead to repayment risks, especially since $1 billion in eurobonds come due in December 2024. Further reforms in public finance and investment management are needed to improve the efficiency of public expenditures.