The World Bank’s new Middle East and North Africa Economic Update, entitled Conflict and Debt in the Middle East and North Africa, shows that lackluster growth, rising indebtedness and heightened uncertainty due to the conflict in the Middle East are impacting economies across the region.

According to the report, MENA economies are expected to return to low growth akin to the decade prior to the pandemic. MENA’s gross domestic product (GDP) is forecast to rise to 2.7% in 2024, which is a tepid increase from 1.9% in 2023. As in 2023, oil importing and oil exporting countries are likely to grow at less disparate rates than 2022, when higher oil prices boosted growth in oil exporters. For Gulf Cooperation Council (GCC) countries, the 2024 growth uptick reflects expectations of robust non-oil sector activity and fading out of oil production cuts towards the end of the year. GDP growth in almost all oil importing countries is expected to decelerate.

The report looks at the economic impact of the conflict in the Middle East on the region. Economic activity in Gaza has come to a near standstill. The GDP of the Gaza strip dropped by 86% in last quarter of 2023. The West Bank has plunged into a recession, with simultaneous public and private sector crises. A recent World Bank report goes into further depth on damages to the Gaza Strip and catastrophic impacts on the people of Gaza.

The economic impact of the conflict on the rest of the region has remained relatively contained, but uncertainty has increased. For example, the shipping industry has coped with shocks to maritime transport by rerouting vessels away from the Red Sea, but any prolonged disruptions to routes through the Suez Canal could increase commodity prices regionally and globally.

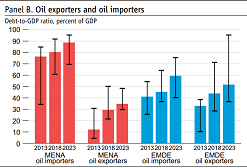

The report also looks at rising indebtedness in the MENA region. Between 2013 and 2019, the median debt-to-GDP ratio for MENA economies increased by more than 23 percentage points. The pandemic made things worse as declines in revenue, together with pandemic support spending, increased financing needs for many countries.

This rising indebtedness is heavily concentrated in oil-importing economies, which now have a debt-to-GDP ratio 50 percent higher than the global average of emerging market and developing economies. Approaching 90 percent of GDP in 2023, oil-importing countries in MENA have a debt-to-GDP ratio almost three times higher than that of oil exporting countries in the region.

The report presents evidence that oil-importing countries in MENA have been unable to grow out of debt or inflate their debt away, making fiscal discipline essential to curb indebtedness. Critically, off-budget items which have played a large role in some MENA economies have been to the detriment of debt and fiscal transparency.

The challenge for oil exporters is one of economic and fiscal-revenue diversification, given the structural change in global oil markets and the rising demand for renewable sources of energy. Overall, MENA economies need to undertake structural reforms, chief among them transparency, to unlock growth and forge a sustainable path ahead.